TL;DR. Charm is the second-order Greek that measures how delta decays as an option moves toward expiration. On Friday afternoons, charm forces dealers to sell stock against heavy call OI and buy stock against heavy put OI. The net imbalance creates a directional drift that has nothing to do with news or technicals. If you can read the charm map at the open, you know what the afternoon will probably do.

Software Automated Research Team | Published 2025-02-19

The Second-Order Greek Nobody Teaches

Every options trader learns delta, gamma, theta, and vega. Few are ever taught charm, the partial derivative of delta with respect to time. Charm sits one level deeper than the standard Greeks, which is why most retail education skips it. That is unfortunate, because charm is responsible for some of the most repeatable intraday patterns in SPX, particularly in the final two hours of every Friday session.

The mechanism is not theoretical. Charm flows are documented in dealer-positioning literature (Garleanu, Pedersen, and Poteshman 2009 first formalised the hedging-flow externality) and they are visible in tick-level price data on every Friday near OPEX. When you see SPX grind in a single direction from 1 p.m. ET to 3:30 p.m. ET with no obvious catalyst, you are almost always watching charm.

What Charm Actually Does

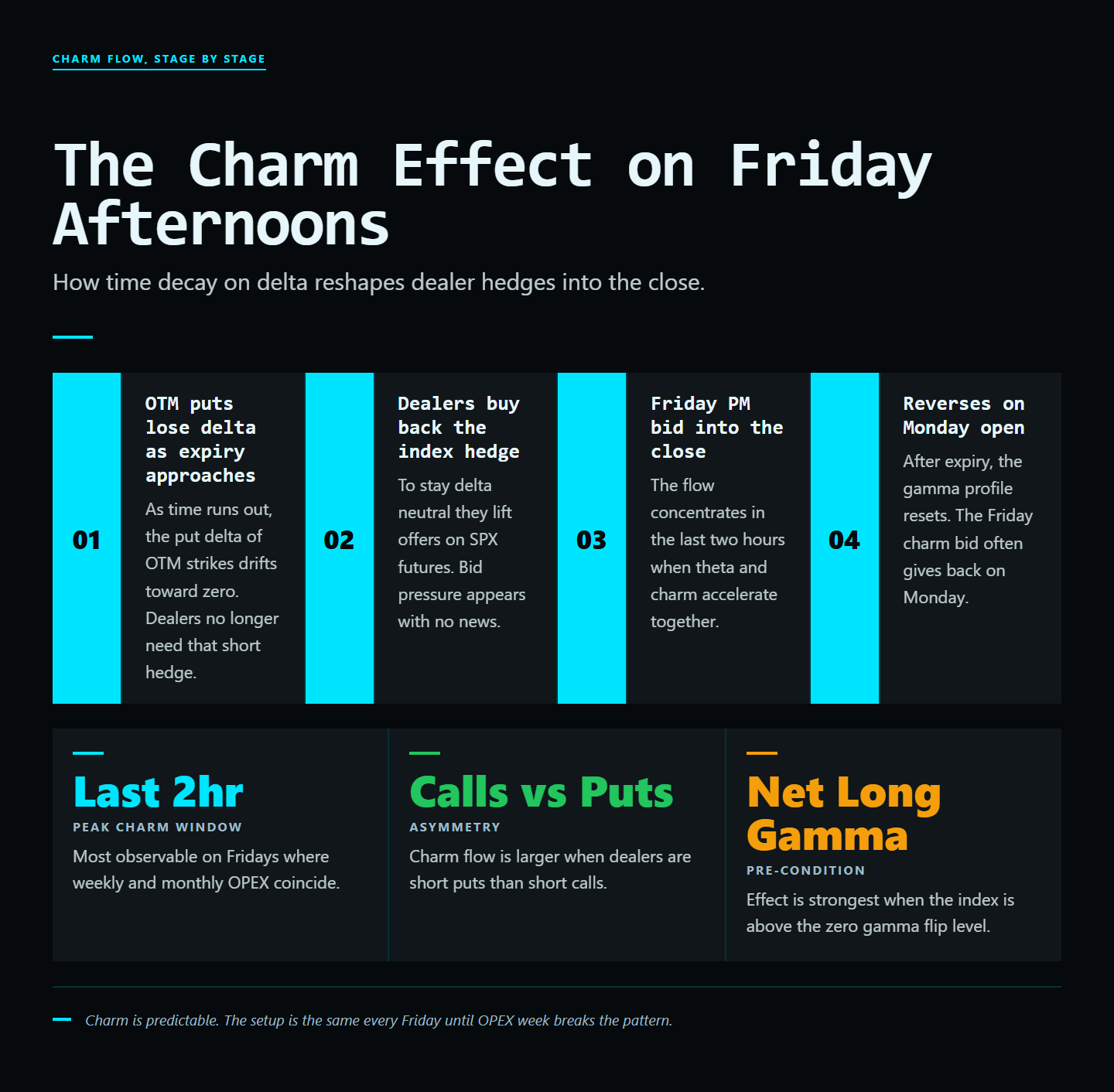

As an option approaches expiration, out-of-the-money deltas decay toward zero and in-the-money deltas accelerate toward 1 (or -1 for puts). This decay is not linear. It is a curve that steepens sharply in the final 24 hours and accelerates almost vertically in the last hour. Dealers hedging short-gamma positions must continuously rebalance against this decay, and the size of that rebalance is precisely what charm measures.

Think of charm as gamma's time-dependent twin. Gamma tells dealers how to hedge against a price move. Charm tells dealers how to hedge against the clock. Both create flows. Gamma flows happen continuously as price moves. Charm flows happen continuously as time passes, even if price does nothing.

Why charm matters more near expiration

Far from expiration, charm is small. Delta on a 30-day OTM call barely moves day-to-day from time decay alone. But on a 0DTE option, charm is enormous. A 0DTE call that is 1% out-of-the-money at 10 a.m. can charm from a delta of 0.30 to a delta of 0.05 by 2 p.m. with no price movement at all. Dealers hedging hundreds of thousands of those contracts must sell stock to neutralize the disappearing delta. That selling is the charm flow.

The Friday Drift Pattern

When the market closes Friday near a heavy call-wall strike, dealers holding short calls have those deltas charm down toward zero through the afternoon. To stay hedged, they sell the underlying. The opposite happens with heavy put open interest. Dealers buy stock as put deltas decay.

Net result: the imbalance between call and put open interest above versus below current price creates a directional drift independent of any news. This is the "charm pin" effect, and it is why so many SPX Friday afternoons look like slow grinds in one direction. The direction is set by the OI imbalance, not by anything you can see on a chart.

The morning calculation

Pull the open interest by strike for Friday's expiration at 9 a.m. ET. Sum call OI above current price. Sum put OI below current price. If call OI dominates, expect a drift lower through the afternoon as dealers sell against decaying call deltas. If put OI dominates, expect a drift higher as dealers buy against decaying put deltas. The magnitude of the drift scales with the OI imbalance. A 3x call-over-put imbalance produces a much bigger drift than a 1.2x imbalance.

Where Traders Get This Wrong

Retail traders often interpret the late-day drift as "trend" and chase it. By 3 p.m. ET, the bulk of the charm flow has already happened. Entering then is buying exhaustion. The charm trade is morning-into-afternoon, not afternoon-into-close. Inside the GammaEdge Discord, the bot publishes a charm map showing where dealer flows have already concentrated and where the residual imbalance still sits. That is the difference between predicting the drift and chasing it.

The two timing mistakes

Mistake one: entering at 11 a.m. on a charm-down day. Charm flow is heaviest from 1 p.m. onward as deltas decay fastest near expiration. Entering too early often means sitting through chop. Wait for the flow to start.

Mistake two: holding into 3:45 p.m. The last 15 minutes of a Friday charm day are often a reversal as profit-taking and end-of-day rebalancing dominate. Exit at the 3:30-3:45 window, not at 3:59.

Three Conditions That Sharpen the Charm Trade

- High open interest concentration. The effect is mechanical. Bigger OI imbalance, bigger drift. If OI is roughly balanced, charm flows cancel out and the afternoon will look choppy.

- Low realized volatility on the day. Charm flows dominate when other flows are quiet. A morning with heavy news flow buries charm under noise. A quiet morning lets charm drive.

- Positive GEX regime. In negative gamma, charm gets overrun by hedging flows in the other direction. Positive-gamma days let charm play out cleanly because dealers are absorbing volatility rather than amplifying it.

A worked example: charm-down Friday

Friday morning, SPX is at 5500. Call OI at the 5510, 5520, 5530 strikes totals 450,000 contracts. Put OI at 5470, 5460, 5450 totals 180,000 contracts. Call-over-put imbalance: 2.5x. GEX is positive at +$1.8B. Realized vol overnight is 0.4%. Conditions: all three sharpening filters met.

Trade plan: short SPY at 11 a.m. as charm flow begins, hold for a drift of 0.4-0.7% lower through the afternoon, exit at 3:30 p.m. ET. Outcome: SPY drifts from 550.00 to 548.20 between 11 a.m. and 3:30 p.m. with three small mean-reversion bounces along the way. Profit at the size you sized for.

This is a textbook charm setup. Members in the GammaEdge community trade variants of this multiple times per quarter, particularly around OPEX where the OI concentration is largest.

Charm around OPEX vs charm on a normal Friday

OPEX Fridays (third Friday of each month) amplify charm dramatically. Monthly options expire alongside the weekly, which means OI concentrations at strike are 5-10x larger than a normal Friday. The charm drift on a monthly OPEX can be 1.5-2x the magnitude of a normal Friday. The flip side: OPEX often comes with macro news (FOMC, CPI, etc.) that overrides charm. Always check the calendar before sizing the OPEX charm trade.

FAQ

Does charm work on stocks other than SPX?

It exists everywhere there is options open interest, but the effect is loudest on the most liquid indices (SPX, SPY, QQQ) where OI is large enough that dealer hedging moves price. On a single name with smaller OI, charm flows can be drowned out by other order flow.

Why is the effect mostly on Friday afternoons?

Because weekly options expire Friday and the delta decay (charm) is steepest in the final 4-8 hours before expiration. Earlier in the week, charm exists but is small. On Friday afternoon, it is dominant.

Can I trade charm without options?

Yes. The charm drift moves the underlying. You can trade SPY shares (or SPY/QQQ futures) around the morning charm map without ever opening an option position.

What kills a charm setup?

Macro news that flips dealer flow. A surprise CPI print, an FOMC pivot, or geopolitical risk-off can override the morning charm posture entirely. Always have an invalidation level on a charm trade.

Sources and further reading

- Garleanu, N., Pedersen, L. and Poteshman, A. (2009). "Demand-Based Option Pricing." Review of Financial Studies. The formal framework for dealer-hedging externalities.

- CBOE research on Friday OPEX behaviour and dealer hedging flows.

- GammaEdge charm-map documentation at gammaedge.com.

Verdict

Charm is not glamorous. It is not a chart pattern, not a sentiment indicator, not a momentum signal. It is a mechanical hedging flow driven by the time-decay of dealer-held options. That is exactly why it works: the flow happens whether the market cares about the news or not. If you can read the charm map at 9 a.m. and act on it at 11 a.m., you are trading the same setup professional desks have known about for decades. If you ignore charm and chase the 2:30 p.m. drift instead, you are the exit liquidity for the desks that did the math.

What to do next

Stop trading the chart. Trade the flow.

WHAT

GammaEdge: the Whop community Taylor Drake runs. GEX dashboard, Discord bot, daily 9 a.m. ET session, wheel + P-Trans+GEX frameworks.

WHY

Same dealer-positioning data hedge funds pay 10x more for, packaged for active retail options traders.

HOW

14-day free trial. $0 charged today. 30-day refund: do not make a $150 trade in month one, get every dollar back.

Affiliate disclosure: GammaEdge is a paid product. We may earn a commission if you join through our Whop link, at no extra cost to you. All editorial assessments above are independent.