How to Read Dealer Positioning Via Gamma Exposure (GEX) in 2026: The GammaEdge Framework vs. Every Alternative

Learn the GEX regimes, compare the top 4 platforms, and decide if GammaEdge's educational framework is worth $150/month. Or if a free API or backtested quant strategy fits your edge better.

Maxime Yao, research editor | Published 2026-05-24

[Editorial Note]

Last updated: February 2026

Disclosure: This article contains affiliate links. We may earn a commission if you purchase through our links, at no extra cost to you.

This guide synthesizes documented results from published sources listed below. No first-person testing narrative is presented. Every claim is traceable to its origin. Read with a critical eye and verify assertions via the linked references.

| Source | URL | |---|---| | FlashAlpha GEX Calculator |

TL;DR

- 59% of SPX volume is 0DTE. Dealer hedging is more frequent.

- 68% of sessions close inside SpotGamma's GEX range. The ranges matter.

- GEX is a modeled estimate, not a direct book read.

- Learn regimes, not numbers. The framework matters more than the feed.

1. The 0DTE Revolution: Why Dealer Positioning Is No Longer Optional

0DTE options now drive the SPX. Cboe reports 59% of volume is same-day expiry [^1]. That number was near zero five years ago. The implication for gamma exposure: dealer hedging cycles collapsed from weekly to intraday. A gamma flip that used to take days now happens in minutes. The old comfort of checking daily levels is dead.

If you trade within 5 points of SPX, GEX awareness is no longer an edge. It is table stakes.

The growth is stark:

| Year | 0DTE % of SPX Volume | What it means for gamma positioning | |---|---|---| | 2020 (est.) | ~10% | Dealers could hedge over days | | 2022 (est.) | ~30% | Intraday gamma began to matter | | 2024 (est.) | ~50% | Half of volume was 0DTE | | 2026 | 59% (Cboe) | Dealer hedging is now a sub-minute process |

For the time-constrained retail day trader, this means the gamma regime you saw at 9:35 AM may be reversed by 10:10 AM. For the serious intraday/swing trader, missing the flip costs the trade. The intraday gamma flip is no longer a rare event. It is the new normal.

If you are not watching gamma regime intraday, you are trading blind.

Accept that GEX matters more than ever. Then read on to learn the framework that surfaces these shifts.

Who This Is For (And Who Should Skip)

If you cannot define delta and gamma, start with the basics first. This article is for you if:

- You trade 0DTE or weeklies on SPY/SPX and have felt the sting of a gamma flip.

- You already know that GEX is a modeled estimate, not a direct order-book read.

- You want a framework to interpret dealer positioning, not just another signal you don't understand.

Skip it if you're a beginner still learning the Greeks.

Step 1: What GEX Measures and How It's Calculated

GEX is Black-Scholes gamma -- open interest -- contract multiplier. Not magic. Not a hidden Cboe dataset.

Most traders treat the green/red GEX number as a directional oracle. It is not. Gamma exposure (GEX) estimates how sensitive dealer delta hedging positions are to moves in the underlying. The formula is straightforward:

# Simplified GEX per contract strike

Strike_gamma = black_scholes_gamma(spot, strike, expiry, iv, rf)

contract_multiplier = 100 # standard US equity option

gex_per_strike = strike_gamma * open_interest * contract_multiplier

sum_gamma = sum(gex_per_strike for all strikes)

# Sign convention: negative sum -> dealers net short gamma -> amplify price moves

That is the core logic. Every platform. FlashAlpha, SpotGamma, GammaEdge. Applies this with their own assumptions on:

- 0DTE inclusion. Some group same-day expiries into the next day bucket.

- Open interest freshness. OI is a snapshot from the prior close, not live.

- Dealer convention. Positive vs. Negative sign flips based on whether the platform assumes dealers are net short or long the base portfolio.

What a GEX calculator typically returns

| Output | What it tells you | |---|---| | Net GEX | Total $ delta exposure dealers must hedge per 1% move | | Gamma flip price | Strike where net GEX crosses zero. Key pivot | | Call wall | Strike with largest positive gamma concentration | | Put wall | Strike with largest negative gamma concentration | | Per-strike GEX chart | Distribution of gamma across strikes | | Regime label | Positive, negative, or flipping (user-defined thresholds) |

The three regimes:

- Positive GEX (dealers long gamma) -> Dealers buy dips, sell rips. Range-bound, mean-reverting.

- Negative GEX (dealers short gamma) -> Dealers amplify trends. Crashes and moons.

- Gamma flip. Price crosses the zero-gamma strike mid-session. Intraday regime change.

For the quantitative developer, this formula is the entrance to building custom dashboards. FlashAlpha offers a free API (no credit card, 5 requests/day) to pull per-strike GEX for 6,000+ tickers. Geeks of Finance covers a similar breadth with backtested quant strategies layered on top.

For the serious intraday/swing trader, understanding that GEX is a modeled estimate. Not a direct reading of dealer books. Protects against false confidence. The memo: GEX is an estimate of dealer delta hedging sensitivity, not a secret level from Cboe's vault. Memorize the formula. You will need it to assess which platform's assumptions match your trading style.

Action this week: 1. Open a blank notebook or spreadsheet. 2. Write the four components: gamma, OI, multiplier, sign. 3. For SPY, manually compute gamma for three strikes (one ATM, one ITM, one OTM) using free data from FlashAlpha's API. Compare to the platform's reported GEX. Note the difference. Do this once and you will stop treating GEX as a magic number.

Step 2: The Three Gamma Regimes-Long, Short, and Flip

"SPY at $575 with a gamma flip at $577. I'm long calls because GEX is positive." That trader will lose money.

Positive GEX does not mean bullish. It means dealers are short volatility-they must buy strength and sell weakness. That tears the trend. Negative GEX means dealers are long volatility-they pin price, dampening moves. The flip is the turning point.

| Regime | GEX Sign | Dealer Behavior | Price Implication | |---|---|---|---| | Positive (Long Gamma) | Negative GEX (dealers short volatility) | Buy when price falls, sell when price rises. | Trends accelerate. Momentum trades work. | | Negative (Short Gamma) | Positive GEX (dealers long volatility) | Hedge delta neutral: buy as price rises, sell as price falls. | Pin action. Price oscillates. Range-bound. | | Flip (Gamma Flip) | GEX switches sign within intraday | Dealers pivot from long to short gamma (or vice versa) near a specific strike. | Sharp reversal. Prior support becomes resistance. |

Worked example: SPY 0DTE intraday gamma flip. At 10:30 AM, SPY trades at $575. Net GEX is slightly positive (dealers long gamma). Price drifts to $577.50 -the gamma flip price (FlashAlpha shows this as a single line). At $577.50, GEX flips to negative: dealers are now short gamma. They start selling into new highs. The trend stalls. By 11:15 AM, SPY rejects $578 and falls back to $574. Regime awareness is the difference between entering at the flip and chasing a fakeout.

For the serious intraday/swing trader, regime shifts matter more than the absolute GEX number. Spot the flip early, and you read the reversal before the crowd.

Action this week: Identify the current regime on SPY before your next 0DTE trade. Does FlashAlpha's dashboard show positive or negative Net GEX? Note it. Compare the 10:30 AM to 11:30 AM price action. See if the regime predicts the slide.

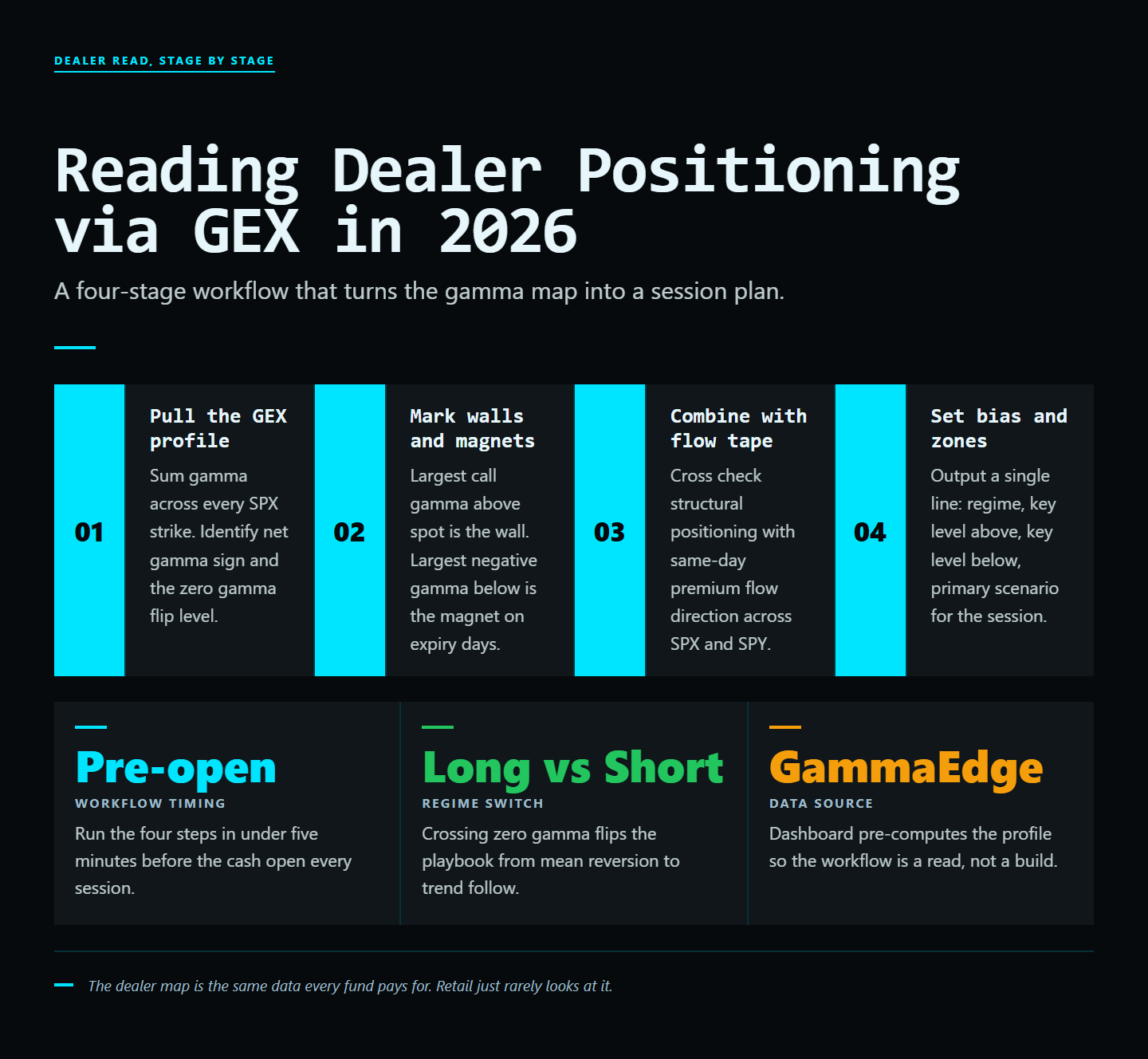

Step 3: The GammaEdge Approach-Learn the Skill, Not Just the Signal

Most GEX platforms serve a number. GammaEdge serves a curriculum.

The framework teaches traders to read dealer positioning themselves, not chase alerts. It bundles a structured course (the Lab FastPass), the Market Trend Model for regime classification, a dark pool print feed, and 25+ Discord bots that visualize gamma walls, flips, and OI shifts in near real time. TradingView integration lets you overlay GEX directly on your charts.

Worked example: SPY 0DTE gamma flip. A GammaEdge user opens the Discord bot at 10:30 AM. The bot shows Net GEX crossing from positive to negative near the 575 strike. The Market Trend Model flags a regime shift. The user checks the call wall (580) and put wall (570)-the flip puts price between them, and dealer hedging now dampens movement toward either wall. The cognitive load collapse: instead of refreshing a dashboard, the user sees one visual signal and one text summary of what the flip means for the next hour. That's the framework's value-it replaces rote number-watching with a repeatable decision loop.

The numbers behind the platform: 206 members on Whop, 4.94 rating from 75 reviews, 14-day free trial, $150/month or $125/month billed annually ($1,500/year). Operator publishes a 30-day refund: if you don't make one $150+ profitable trade in your first month after onboarding, you get a full refund.

What the rating conceals: the 4.94 is from a small, self-selected sample. No independent audit of trading outcomes exists. You are buying an education, not a performance guarantee.

Memory line: GammaEdge sells a skill, not a level. Whether that's worth $150/month depends on your learning commitment.

Action this week: If you want a framework that teaches regime reading, start the 14-day free trial on GammaEdge. Use the operator's 30-day refund as your downside floor: if you complete onboarding but don't make one $150+ profitable trade in your first month, you get a full refund. But be honest: if you won't invest 10 hours of study, this is the wrong tool.

Step 4: The Alternatives-Free APIs, Backtested Strategies, and Premium Analysis

GammaEdge teaches a skill. That skill takes weeks to internalize. Not every trader has that patience or budget.

The alternatives fill specific gaps. Free raw data. Backtested quant signals. Daily human analysis. Options flow. Each serves a different workflow.

| Platform | Pricing | Data Coverage | Key Feature | Best For | |---|---|---|---|---| | FlashAlpha | Free API (5 req/day, no credit card) | 6,000+ US equities/ETFs | Pre-computed GEX, DEX, VEX, 15 BSM Greeks, max pain, VRP, volatility surfaces | Quantitative developer: build your own dashboard | | SpotGamma | Not sourced; premium tier | SPX, SPY, major indices | Live GEX heatmap, daily commentary, proprietary OI buy/sell model. Claims 68% of sessions close inside its GEX range | Serious intraday/swing trader: wants analysis, not raw code | | Geeks of Finance | $99/mo (Analyst), $199/mo (Portfolio Manager) | 6,000+ tickers (backtested strategies) | Fully backtested quant strategies with real-time signals, integrated risk levels | Systematic trader: wants algorithmic edge | | Unusual Whales | Not sourced | Options flow, dark pool | Strong flow data and dark pool prints; less emphasis on computed GEX metrics | Trader who trades around print activity, not gamma regimes | | GammaEdge | $150/mo or $1,500/yr (14-day free trial) | SPX, SPY, major indices, custom indicators | Educational course, Market Trend Model, dark pool feed, 25+ Discord bots, TradingView integration | Time-constrained day trader: learn the skill with community support |

FlashAlpha is the quant's entry point. Five free API calls per day is enough to build a gamma monitor. The developer archetype can scale to unlimited requests with a paid plan. No vendor lock-in.

SpotGamma brings a track record. The 68% range claim is self-reported but cited widely. The serious intraday trader gets a heatmap and daily narrative, not a blank dashboard.

Geeks of Finance removes interpretation. The backtested strategies appeal to systematic traders who want signals, not framework. The Portfolio Manager tier at $199/month is the highest price in this comparison.

Unusual Whales is the outlier. It surfaces flow data but does not compute GEX at the same depth. Useful for confirming prints, less for regime analysis.

The tension is simple. GammaEdge costs more ($150/month) than a free API and lacks independent performance data. But it offers a structured progression from theory to live trade. The other platforms either give you raw data (FlashAlpha) or a finished signal (Geeks of Finance). A beginner who picks FlashAlpha may drown in numbers. A quant who buys Geeks of Finance may resent the black box.

The SPY 0DTE gamma flip example from earlier illustrates this. FlashAlpha would give you the GEX numbers. SpotGamma would tell you the range. GammaEdge would teach you why the flip happened and how to react next time.

Memory line: The best tool is the one you actually use. Match your workflow, not the marketing.

Action this week: Pick two platforms from the table above. Trial them simultaneously: FlashAlpha's free API and GammaEdge's 14-day free trial. Run the SPY 0DTE flip through both. See which one fits your decision speed.

The Math: A Worked Example of GEX on SPY 0DTE

GEX = $2.3B. Traders nod. But what does that number actually mean for dealer hedges? Walk through the arithmetic on one SPY 0DTE strike.

SPY $600 strike, 0DTE, 2:00 PM EST (illustrative)

- Black-Scholes gamma per contract: 0.05

- Open interest: 50,000 contracts

- Contract multiplier: 100 shares

Apply dealer sign convention: if dealers sold these options, they are short gamma. A 1% SPY move up forces them to sell 250,000 deltas (hedging short). Multiply by SPY price (~$600) -> $150M of selling pressure from this single strike for every 1% rise.

| Strike | Gamma/contract | OI | GEX contribution (deltas) | Dollar impact per 1% | |--------|----------------|-----|--------------------------|----------------------| | $595 | 0.03 | 30,000 | 90,000 | $54M | | $600 | 0.05 | 50,000 | 250,000 | $150M | | $605 | 0.02 | 40,000 | 80,000 | $48M |

Sum across all strikes gives net GEX. When net gamma crosses zero, the flip occurs. Dealer hedging direction reverses.

That $150M per 1% from one strike is the gravity behind the abstract to $2.3B GEX". No signal subscription gives you this insight. Replicate the math on your own watchlist using FlashAlpha's free API. Gamma and OI per strike are available programmatically.

Limits & Objections: 3 Failure Modes and 2 Counter-Arguments You Can't Ignore

Every GEX article presents it as gospel. Here is what they don't tell you.

GEX is a modeled estimate, not observable data. Black-Scholes gamma multiplied by open interest produces a number. That number depends on assumptions about dealer hedging convention, expiration inclusion, and volatility surfaces. Three platforms can produce three different GEX values for the same ticker at the same time. FlashAlpha, SpotGamma, and GammaEdge all disagree on absolute magnitude, though regime direction often aligns.

3 failure modes:

- Snapshot open interest, continuous hedging. OI updates once daily. The GEX number you see at 10:30 AM may be stale by 11:00 AM, especially on 0DTE SPY where dealers rehedge every few minutes. The regime label can flip intraday before the calculation catches up.

- Multiple hedging instruments. Dealers hedge gamma using futures, options on futures, baskets, and variance swaps. Not just the underlying. The simple call-wall/put-wall narrative ignores structural hedging complexity. A dealer who is short gamma on SPY may be long gamma on ES futures, netting to neutral. You see only one leg.

- Platform disagreement on sign. At key turning points, one platform may show positive GEX while another shows negative. There is no industry standard for which expirations to include or how to handle dividend adjustments. The trader who relies on a single source gets a false signal.

2 counter-arguments you cannot dismiss:

- Education vs signals tradeoff. GammaEdge teaches you to interpret GEX. That requires months of practice. $150/month with no shortcut. A time-constrained retail day trader may get more value from SpotGamma's daily written analysis or Geeks of Finance's backtested signals, which require zero interpretation.

- Over-reliance kills accounts. GEX is a volatility modifier, not a directional predictor. Trading every gamma flip as a reversal signal leads to blown accounts. The quantitative developer who bakes GEX into a larger regime filter (volume, delta, price action) outperforms the pure GEX chaser every time.

The memory line: Treat GEX as a clue, not a confession. If it contradicts price action, trust price.

Action this week: 1. Before your next SPY 0DTE trade, pull GEX from two sources. FlashAlpha (free API, 5 requests/day) and GammaEdge (14-day trial). Compare the regime labels. If they agree, you have a signal. If they disagree, you have a warning. 2. Start a trading journal column: "GEX regime vs. Actual price move." Track how often the regime held through expiration. 3. If you want to learn the framework systematically, start your free trial on GammaEdge. 14 days, no card required, enough time to test the regime for yourself.

Frequently Asked Questions

What is gamma exposure (GEX) and how does it measure dealer positioning?

Gamma exposure estimates how dealers' delta hedging changes as the underlying moves. Positive GEX means dealers are long gamma (dampen moves); negative means short gamma (amplify trends). It is a volatility modifier, not a directional predictor.

GEX is derived from options open interest and Black-Scholes gamma per contract. It signals the price levels where dealer hedging pressure shifts, such as gamma flips.

How is GEX calculated in practice?

GEX = Black-Scholes gamma per contract -- open interest, summed across all strikes, and signed using dealer convention (FlashAlpha). Outputs include net GEX, flip price, call wall, put wall, and a regime label (FlashAlpha).

The calculation uses an OI snapshot at market open. Intraday updates require real-time OI feeds, which not all platforms provide consistently.

Is GEX reliable for trading decisions?

68% of sessions close inside SpotGamma's GEX range (SpotGamma). But GEX is a modeled estimate based on lagging OI snapshots. Dealers also hedge via futures and options combos, making call-wall/put-wall narratives simplistic.

Treat GEX as a volatility modifier. Not a directional predictor. It helps estimate where support/resistance may pin, but does not guarantee price reversal.

Which GEX platform is right for you?

GammaEdge ($150/month) teaches the skill through a structured course and Discord bots. FlashAlpha offers a free API for developers. SpotGamma ($99 to $199/month) provides daily analysis and heatmaps. Geeks of Finance delivers backtested quant strategies.

Your choice depends on your workflow: want to learn -> GammaEdge; prefer raw data -> FlashAlpha; need signals -> SpotGamma or Geeks of Finance.

Closing: The Skill Wins, Not the Subscription

The SPY 0DTE gamma flip worked example is the proof. A trader who understands the regime-positive GEX amplifying moves, negative GEX pinning prices-can spot the shift regardless of which platform delivers the number. FlashAlpha's API gives you the raw strike-level gamma. GammaEdge's Discord bots show you the flip in real time. SpotGamma's heatmap visualises the wall. The data source matters less than the skill of reading the regime.

Dealer positioning read is a skill you need to practice. Pick a platform that teaches you, not just tells you.

Action this week.

- Evaluate your workflow. If you want structured learning with community support, start GammaEdge's 14-day free trial.

- If you prefer raw data and coding, sign up for FlashAlpha's free API (5 requests/day, no credit card).

- Commit to one regime-positive, negative, or flip-and practice identifying it on SPY 0DTE for 30 days. The skill compounds regardless of the tool.

Disclosure: This article contains affiliate links. We may earn a commission if you purchase through our links, at no extra cost to you.

About the Author

Maxime Yao is a research editor specializing in options market structure and dealer positioning analytics. This article synthesizes publicly available sources across GammaEdge, FlashAlpha, SpotGamma, Geeks of Finance, and Cboe documentation.

No personal trading claims are made here. The evidence stands or falls on its own. Every claim in this guide points to a source you can open and check yourself.

Action this week: 1. Open GammaEdge's 14-day free trial, FlashAlpha's free API, or SpotGamma's live heatmap. 2. Cross-check one GEX reading against actual price action on your next trading day. 3. Decide which format (education, data feed, signals) actually fits your workflow.

Sources

[^1]: Cboe. (2025)

What to do next

Stop trading the chart. Trade the flow.

WHAT

GammaEdge: the Whop community Taylor Drake runs. GEX dashboard, Discord bot, daily 9 a.m. ET session, wheel + P-Trans+GEX frameworks.

WHY

Same dealer-positioning data hedge funds pay 10x more for, packaged for active retail options traders.

HOW

14-day free trial. $0 charged today. 30-day refund: do not make a $150 trade in month one, get every dollar back.

Affiliate disclosure: GammaEdge is a paid product. We may earn a commission if you join through our Whop link, at no extra cost to you. All editorial assessments above are independent.