TL;DR. 0DTE options now account for more than half of SPX options volume on a typical day. Their explosive gamma profile makes them the single most dealer-hedge-driven product on the market. Traders who treat them like longer-dated contracts blow up. Traders who treat them as a positioning game first and a chart game second extract a real edge.

Software Automated Research Team | Published 2025-03-04

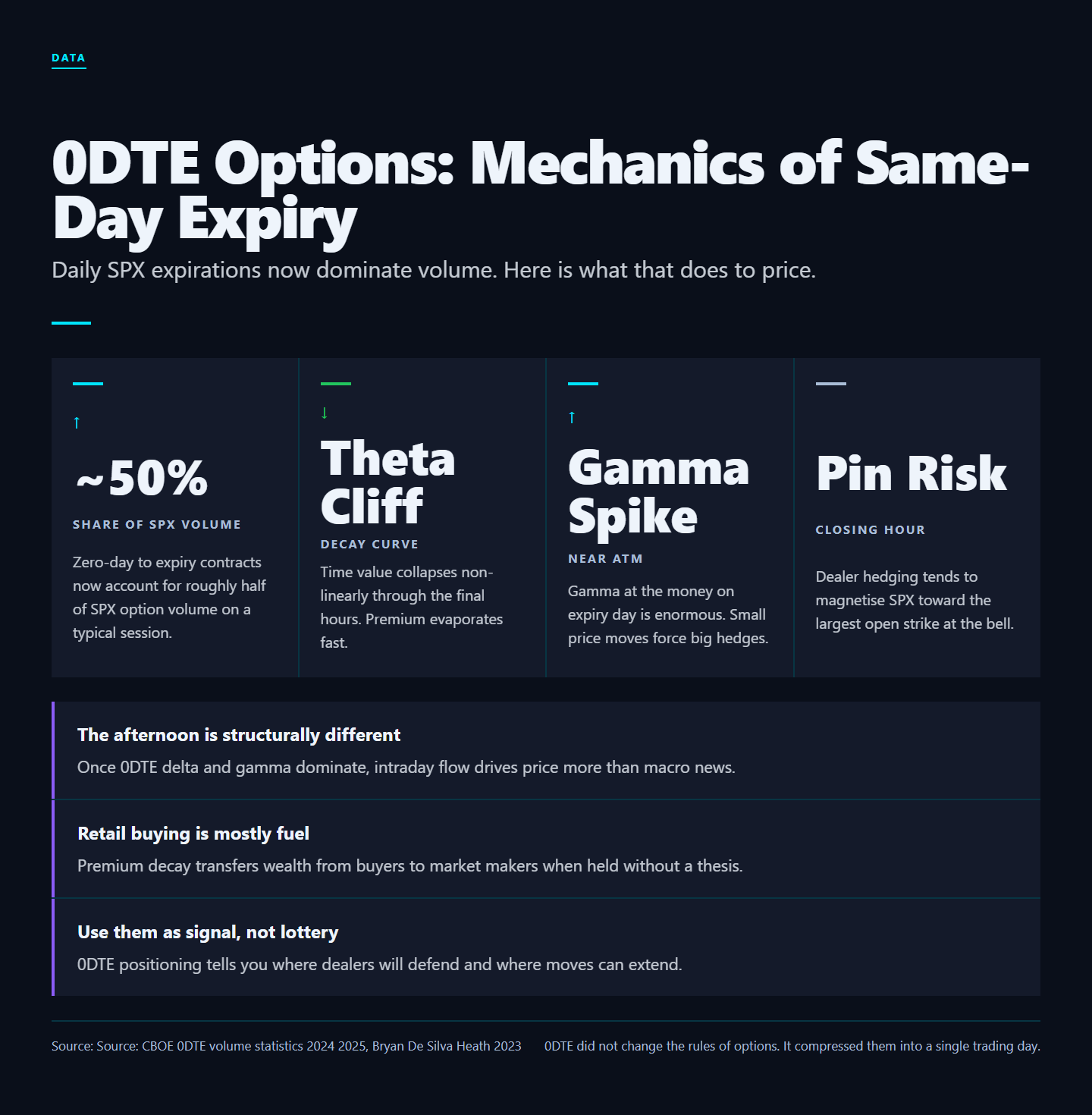

From Niche to Half the Tape

In 2022 the CBOE expanded SPX weekly expirations to every weekday. What started as a niche product (Tuesday/Thursday SPXW) is now the largest single segment of options volume. CBOE's own monthly volume reports show 0DTE SPX accounting for more than 50% of total SPX options volume in most months since late 2023. The result is that the entire intraday character of the index has shifted. Pre-2022 SPX was driven mostly by monthly OPEX dynamics. Post-2022 SPX is driven by daily expiration mechanics.

That shift is not abstract. It changed how dealers manage gamma exposure, how charm flows compound through the week, how 2 p.m. ET dealer rebalances happen, and which strikes act as magnets on a given day. If you trade SPX or SPY in 2026 and beyond and you do not understand 0DTE mechanics, you are reading the tape with one eye closed.

Why 0DTE Is Different

Same-day options have effectively zero theta runway and gamma values that explode as you approach the money. A small move in SPX produces enormous delta changes on at-the-money 0DTE contracts. For dealers selling these options, the hedging requirements are immense, and they happen in seconds, not hours.

Gamma in a closed-form example

A 30-day call at the money has a gamma per contract of roughly 0.02. A 0DTE call at the money has a gamma per contract of roughly 0.20 or higher in the final two hours. That is a 10x increase in hedge intensity per dollar of move. Multiply across 200,000-500,000 contracts of dealer-held 0DTE inventory and you get hundreds of millions of dollars of forced flow per 0.1% SPX move. Those flows are themselves the price action.

The theta cliff

0DTE theta accelerates to near-infinity in the final 30 minutes. A long 0DTE call worth $1.20 at 3 p.m. can be worth $0.10 by 3:45 p.m. on flat price. This is why 0DTE is unforgiving to long premium holders: you are not trading the underlying, you are trading the clock, and the clock is always faster than your conviction.

The Three Things That Actually Matter

1. Where the heavy strikes are. 0DTE walls form fast and break fast. The biggest call and put strikes near current price become intraday magnets and barriers. Inside GammaEdge, the bot updates these every minute. Without a tool like that, you are trading blind against participants who can see exactly where you will fail.

2. The opening flow. The first 30 minutes of trade often sets the day's gamma posture. Heavy opening call buying flips dealers short gamma, which causes the day to trend rather than range. Heavy opening put buying does the same in the other direction. Read the opening flow and you have read most of the day's character.

3. The dealer recovery zone. Mid-day, dealers often unwind portions of their morning hedge as charm starts to compress delta. This creates predictable retracements at predictable times, usually between 11:30 a.m. and 1 p.m. ET. Members who know this pattern enter against the morning trend at that zone with defined risk.

The 0DTE day in four phases

Phase one: 9:30-10:00 a.m. ET (opening)

Opening flow is decisive. Dealer gamma profile is set here. Range expansion or compression for the rest of the day is largely predictable from this window. Trade only if your edge is in reading the flow, not in catching the open.

Phase two: 10:00 a.m.-12:00 p.m. ET (morning trend)

The most tradable window. Gamma is well-defined, charm has not yet kicked in heavily, and intraday news catalysts (econ data at 10 a.m., etc.) are absorbed. Best for directional trades aligned with the morning gamma posture.

Phase three: 12:00-2:30 p.m. ET (charm + lunchtime drift)

Volume dies, charm flows take over, and the afternoon's directional bias firms up. Mean-reversion at intraday levels often works. Premium sellers thrive if positive GEX. Premium buyers should be patient.

Phase four: 2:30-4:00 p.m. ET (close + dealer rebalance)

The closing dealer rebalance is the most violent flow of the day. 0DTE strikes near the money pin, then break, then pin again as dealers manage residual exposure. Most blow-ups happen here because retail traders chase the late move.

What Kills Retail 0DTE Traders

Three patterns account for most blow-ups:

- Chasing breakouts late. By the time SPX breaks a gamma wall, the move has already happened. The dealer hedging that drove the break is finished. Buying the break is buying the exhaustion.

- Holding too long. Theta on 0DTE compounds against you exponentially in the final two hours. A 2:30 p.m. entry that needs another 1% in your direction to be profitable will almost always lose to theta even if you are directionally right.

- Trading without positioning data. 0DTE is a positioning game first, a chart game second. Without GEX, OI, and dealer-hedge mapping you are trading on chart-pattern hope against participants who can see your stops.

- Sizing for the home run. 0DTE option payoffs are convex. A small directional move can 5x or 10x a long-call position. That ratio attracts retail traders to over-size. A blown-up account does not get to make the next trade.

The Framework We Teach

Inside the GammaEdge community, 0DTE setups follow a checklist: gamma regime -> walls identified -> opening flow confirmed -> entry near a level, not through it. The bot does the data work. The members do the execution. The result is a consistent edge in a product where most retail traders are net donors.

The four-step morning routine

- 9:00 a.m. ET. Pull the overnight GEX update. What flipped from yesterday's close? Where is zero-gamma?

- 9:15 a.m. ET. Identify the call and put walls. Which strikes have the heaviest 0DTE OI? Those are your structural ceiling and floor.

- 9:35 a.m. ET. Watch the opening flow. Heavy call buying suggests a trending day, heavy put buying suggests downside acceleration. Mixed flow suggests a range.

- 10:00 a.m. ET. Take your first trade only if all three signals agree. If GEX says range, walls say tight, and opening flow says mixed, sell premium near the walls. If GEX says trend, walls are far apart, and opening flow is one-sided, buy directional structure aligned with flow.

FAQ

Can I trade 0DTE on stocks other than SPX/SPY?

0DTE-style same-day expirations exist for QQQ, IWM, and a handful of single names (NVDA, TSLA, etc.) with daily options, but the gamma dynamics are most pronounced on the indices because dealer-side concentration is largest there.

What size should I trade 0DTE at?

Smaller than you think. The convex payoff invites over-sizing. A reasonable starting framework: never risk more than 1% of account on a single 0DTE structure, and cap total 0DTE exposure at 3-5% of account per day.

Are 0DTE spreads better than single legs?

Almost always yes. Defined-risk spreads (verticals, condors, butterflies) eliminate the catastrophic-loss tail. Single-leg 0DTE long calls and puts are the highest-variance retail trade on the board. Spreads cap the loss and force position-sizing discipline.

How does 0DTE interact with VIX?

0DTE volume has changed how short-dated volatility prices. Realized SPX volatility has converged with 1DTE implied volatility since 2023, suggesting dealers are effectively pricing the next-day flow into the curve. VIX (which is 30-day forward) is less affected.

Sources and further reading

- CBOE monthly volume reports on SPX 0DTE share of total SPX options volume.

- JP Morgan equity derivatives research on 0DTE dealer-hedging flows.

- Bryan, De Silva, and Heath (2023) on retail option-trading costs.

- GammaEdge 0DTE setup documentation at gammaedge.com.

Verdict

0DTE is not a free lottery ticket and it is not a doomed-to-lose product. It is a positioning game with measurable edges for traders who do the work and a guaranteed losing game for traders who treat it as a chart-pattern bet. If you cannot articulate the gamma regime, name the walls, and read the opening flow inside the first 30 minutes, you should not be trading 0DTE. If you can, the daily flow is a reliable hunting ground.

What to do next

Stop trading the chart. Trade the flow.

WHAT

GammaEdge: the Whop community Taylor Drake runs. GEX dashboard, Discord bot, daily 9 a.m. ET session, wheel + P-Trans+GEX frameworks.

WHY

Same dealer-positioning data hedge funds pay 10x more for, packaged for active retail options traders.

HOW

14-day free trial. $0 charged today. 30-day refund: do not make a $150 trade in month one, get every dollar back.

Affiliate disclosure: GammaEdge is a paid product. We may earn a commission if you join through our Whop link, at no extra cost to you. All editorial assessments above are independent.